Bad wheat harvest for Russia; US focus moves to soya

Humphrey Feeds Commodity Report, 28 August 2012: The US maize disaster is old news. The US focus has moved to soya.

This week Russia’s SovEcon announced the worst wheat harvest for 9 years, at 39-41mt, due to drought. Wheat yields are about 2t/ha. Russian exporters appear to be particularly active and competitive, in a rush to beat the forthcoming tariffs? It is possible that Russia only has 6mt to export this year, rather than the 21mt in 2011-12. Based on current exports, Russia will run out of wheat in September. The rumour says that if Russia imposes export restrictions, so will the Ukraine. Individual Black Sea countries cannot be exposed.

Western Australia is too dry, their wheat needs rain; and analysts are reducing yields. So three of the largest cereal exporters in the world, will have experienced problems. Cereal ‘liquidity’ in terms of global flows could get sticky this year.

Worst possible timing? Just as the world needs a massive South American soya and maize crop, 1mt of fertilizer is stuck at Brazilian ports due to poor infrastructure, rain and strikes. Although a massive agricultural exporter, Brazil has to import 80% of its fertilizer – well, no-where is perfect. Earlier this month there were 126 ships queuing to unload at Paranagua, and 80 ships at Santos. The queue is about 48 days long, with a daily cost of $40,000. Ouch!

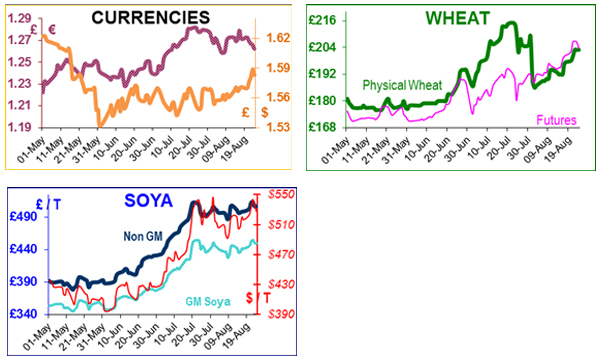

The UK wheat market looks as if it might be complicated this year. Wheat in futures stores has to be 72 bushel, but the wheat traded will generally be lower. So a two or three-tier market will probably develop, where feed wheat will trade according to its bushel. Towards the end of the last harvest year, the flour millers had an easy job, all they had to do was buy good quality feed wheat; then in July it ran out and they got caned.

In the process, the normal carry-in of feed wheat to this harvest year was diminished. If the wheat yield is lower than normal, then the exportable surplus could be less than 1mt, so we will need to import. Flour millers have already started importing French and German wheat to meet their specification, as there is only an £8/t difference between French and UK, which just about pays for the ferry.

Futures stores and feed millers may well be tempted to do the same. No doubt Ensus & Vivergo are trialling low bushel wheat to see if they can clean up, otherwise both are close to ports so they too can import. UK wheat prices are well supported and have been steadily rising over the past three weeks. If all the wheat had been harvested in a week, we may well have seen a harvest-drop in prices. But this year, it has been a harvest dribble, as probably only 15% has been harvested. Prices are reflecting these challenges, with the key position of November peaking at £206 delivered to the mill.

The annual US Pro Farmer Crop Tour started Monday and finished on Friday, with regular bulletins. With yields so variable, it was a volatile trading week.

The world has not experienced a double successive crop failure in the recent past, when supply and demand has been so evenly matched. The world is still smarting from the loss of 20mt of South American soya; if the US losses are significant, soya bean prices could go 20% higher yet. That will ‘ration’ demand, but it will be the poorer societies that will be hardest hit. As the graph shows, soya prices matched recent peaks of over £450 for GM source, and a £60 premium for Non GM soya.