The cumulative solar photovoltaic (PV) capacity installed in the United Kingdom (UK) is forecast to exceed 10 gigawatts (GW) by the end of the first quarter of 2016. New capacity deployment will be driven by more than 100 project developers, 50 EPCs (engineering, procurement and construction companies) and 40 institutional investors, according to the new Solar Media Limited Top-500 UK Database report.

Finlay Colville, Head of Market Intelligence at Solar Media added, “The UK is currently the most vibrant market for solar installations in Europe, due to attractive investment returns from Renewable Obligation Certificates (ROCs) available for large-scale solar projects. Coupled with softness in market demand from mainland Europe, almost every global solar supplier is either active within the UK today, or looking to enter quickly in the next few months.”

When the UK’s utility-scale solar sector started in 2011, there were only a few project developers and EPCs in the market. Over the past four years however, the number of companies participating in UK solar has growth rapidly. During the first three months of 2015, 2.3GW of new solar farms were completed, spread across more than 85 project developers, 60 EPCs, and 50 completed site owners.

“The increase in solar companies active in the UK’s large-scale sector has been boosted by the arrival of experienced European companies, benefiting from legacy market growth in Spain, Germany and Italy. Also, the UK market has seen domestic onshore wind developers turning to solar for diversified revenue streams, and an increasing number of Asian companies acquiring sites in part to secure in-house module supply channels,” added Colville.

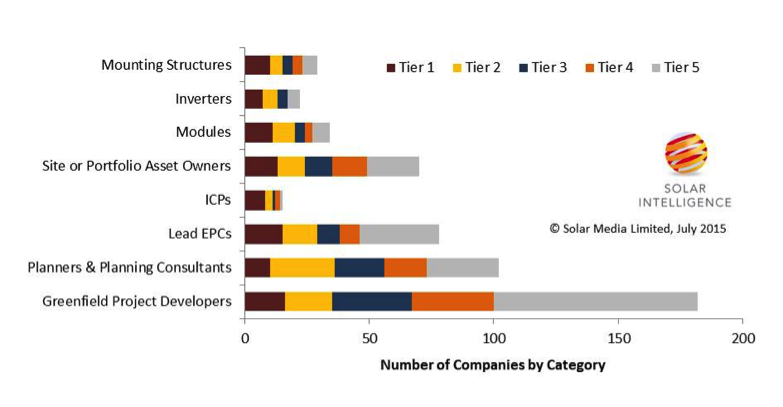

Figure: Breakdown of top 500 companies active in the UK ground-mount solar sector, ranked from Tier 1 (highest market-share) to Tier 5 (lowest).

Source: Solar Media Limited Top-500 UK Database report, July 2015.

More than 80% of new capacity forecast to be built in the UK before 1 April 2016 is expected to come from solar farms rated just below 5 megawatts (MW), in order to qualify for accreditation at 1.3 ROCs/MWh. In the 12 months to 31 March 2015 - when there was no capacity restriction on solar farms - the average size of a large-scale site was nearly 12MW.

This decrease in average solar farm size is forcing developers to scope out a greater number of new sites, in order to meet internal deployment targets over the next nine months, and is creating a more fragmented and diversified supply chain, compared to previous fiscal years. However, there are still sites awaiting construction that are greater than 5MW, having satisfied the government’s ‘grace period’ criteria, imposed following policy changes to the RO scheme last year.

According to the Top-500 UK Database report, the greatest number of companies active in the market is at the project development phase (more than 150), working alongside about 100 key planners or planning consultants. More than 75 lead EPCs are now competing for business from these developers, with about 40 pure-play investment portfolios seeking to acquire completed sites.

“With just nine months to go before the 1.3 ROC year ends, EPCs and component suppliers will need to expand working relationships across the full range of developers and investors that typically specify the supply chains used during construction,” noted Colville. “While policy changes after 1 April 2016 cannot be discounted, having new customers and suppliers will also help in the run up towards the scheduled closure of the RO scheme for solar on 31 March 2017.”