Humphrey Feeds weekly feed report - 22nd August

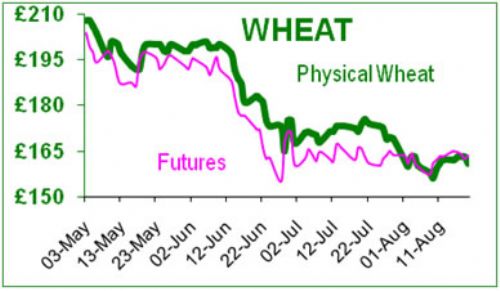

In terms of the weakest link, Black Sea wheat prices are the lowest in the world at $30/t less than Paris, as a result it is believed that the Russkies will have exported over 3mt this month. It is thought they are in a hurry to sell now, to accumulate $s before the potential for winter ice slows their export trade. Indeed the fear of logistical problems to beat the frozen winter has lead to some buyers choosing to buy from warmer climes, particularly as freight costs have risen to service this trade. UK and EU exporters are starting to be concerned that they have few deals on the books. November futures wheat is about ’163.50.

US farmers are able to claim ’preventative planting’ insurance from the USDA for land they had planned to plant, but were unable to do so because of drought or flooding. It would appear that initial claims have been made for 10m acres, which are about 10% more than expected, and mainly affects cotton and spring wheat (durum). Partly fuelled by the unplanted acreages and the possible reduction in maize plantings, December maize futures jumped through the $7.20/b barrier (beating the previous record high in June) and a challenge of $8/b is expected. As US maize has been the driver for UK wheat, it will be interesting to see if the end-of-year old crop maize shortage and fear of reduced production will support new crop UK and EU wheat. If maize prices do increase, then so will soya ’ both are tied together in multiple apron-strings - the ’battle for acres’, energy and biofuels, and in commodity baskets traded by the funds. Similarly US maize and wheat are tied by the same factors, and both can be used to make animal feed; which suggests that the price differentials between these cereals will remain small.

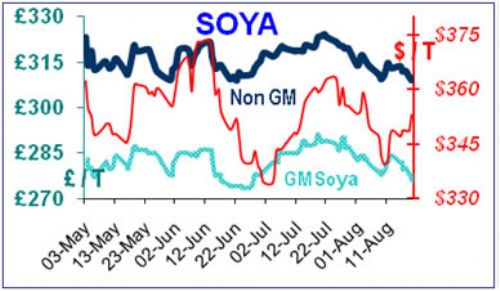

The weekly report of Commodity Futures Trading Commission (CFTC) showed that during the recent financial crisis, the soya positions held by the funds dropped by 47,238 contracts (6mt) to 64,188 contracts (9mt); the largest weekly drop since 2006. Interestingly, almost all the contracts were purchased by the trade, who obviously thought that the cheaper prices were a ’buy’. There is speculation that China was one of the buyers. China believes it will only harvest 13.5mt of soya this year due to drought (15.1mt last year); and the USDA guesses 14mt. China also plans to sell 4mt of soya from its reserves by which time it will only have 1.4mt left in stock according to officials at the China Grain Reserves Corporation. The outside world believed that China only had 3.5mt in stock to start with! If the USDA’s view of the US soya harvest is correct, then global soya supplies will be tight this year; particularly if China’s demand is as anticipated, plus making up the shortfall of its smaller harvest as well as having to replenish its reserves. China already buys about 25% of US’s entire soya crop. The USDA believes China will need to import 56.5mt this coming year (52mt this year).

The question remains as to why China would want to sell such a large percentage of its soya stocks ’ is this is stock rotation? Or is it making room to store more domestic maize, as imported maize is so expensive? China’s population of 1.3bn continues to move from the fields to cities; and as its economy improves, the middle class sector is expanding, eating better, eating more meat and drinking more alcohol so the demand for maize is increasing. In July China bought 500,000t of US maize, so perhaps they need somewhere to store it? Some food strategists believe China will become the US’s main buyer of maize within a few years.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.