Humphrey Feeds weekly feed report - 27th August

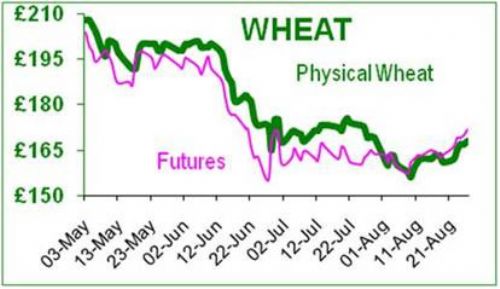

UK November futures closed at £163.55 last Friday, which was followed by two up days £2.45 and £3.00, a no change day, then £1 then £1.75. However soya bean meal stole the show this week, after Fridays close at $354/short tonne, Monday closed at $362, and Tuesday at $368, ending the week at $376, moving through to top of its recent range. It is that volatile time of year when the trade starts navel-gazing and predicts yields on the basis of the outcome of the battle for acres, the weather, plantings and crop tours. Current chatter is about low maize yields, the effect of the weather on maize and soya, and the USDA’s penchant for manipulating the data (or just plain getting it `wrong’). From a strategic point of view, there is so much noise it is impossible to ascertain an overall picture. An analyst would have a better chance of being right by reading tea leaves or chicken entrails! Overall maize and soya prices are relatively high, and the outside markets are teetering on recession, so anything could happen. In terms of positioning, the funds are long and the commercials are short of agricultural commodities: traditional funds are net long of about 80,000 soya, 23,000 soya bean meal, and 290,000 maize contracts; index funds are believed to be net long of 117,000 soya bean, 11,000 soya bean meal, and 224,000 maize and 175,000 wheat contracts; the trade are net short of 448,000 maize, 130,000 wheat and 173,000 soybean contracts.

Last year the FSU experienced a drought and produced only 81mt wheat of which it exported 14mt before the embargo. This year it is expected to produce 107mt and could export 33mt, some 19mt more than last year! Last year global wheat exports were 130mt, so the non-FSU countries exported 116mt. This year the USDA expects global exports to be 131mt, so the non-FSU countries will export only 98mt, some 18mt less than last year. This can only mean that the major exporters Australia, Canada, US and EU will export less wheat, and probably not in equal proportions.

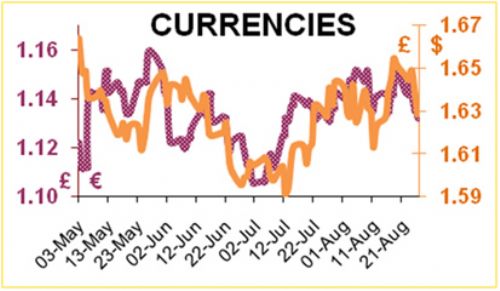

From the investor viewpoint, there are five main types of assets: commodities, cash, property, bonds and company shares. With the exception of commodities, all these assets not only have inherent value but also produce a ’dividend’ in that the investor is paid to hold them. Cash lent to a bank gives interest, property gives rent, bonds give interest, and shares give dividends. Commodities are unsophisticated assets reliant solely on their inherent value, which have been in the ascendant in recent times due to supply and demand, and due to QE. It would appear that QE has been used by the banks and funds to significantly invest in commodities which have added to price inflation, damaging consumer spending and slowing global growth – the exact opposite of its intention. As inflation is now running at 4.4%, the Bank of England is unlikely to approve further QE. If the Fed also declines to launch QE3, then commodities may lose their sex appeal, and values may drift.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.