Humphrey Feeds weekly feed report - 15th August 2011

The turmoil of stock exchanges dominated everything this week, with ugly rumours about France and its biggest banks. So commodities took a back seat until the USDA’s report on Thursday, which announced a reduction of yields of both US maize and soya, and maize went limit up ($0.30/b), and soya jumped $0.33/b. Maize production is estimated to be 12.9bb, which is 4% higher than last year, the 3rd biggest ever crop, but still 1% lower than the trade expected. The maize carry out next year will be larger than expected (a reduction in exports and less bioethanol) however at only 714mb (940mb this year) it will be the lowest stock for 16 years. Soya production is forecast at 3.06bb, a fall of 8% from last year and about 4mt lower than the trade expected; but it is too early to predict soya yields. The soya carry out will be 230mb this year. The current soya to maize price ratio also favours US farmers planting more maize next year.

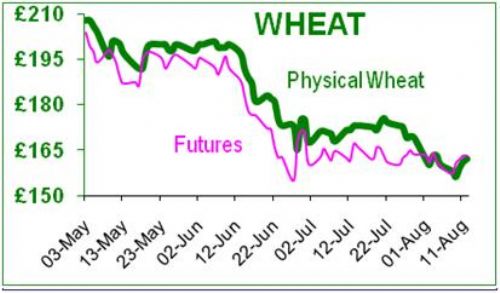

UK Nov futures wheat opened on Monday at £158.50, jumped about £3 on Tuesday due to stock exchange antics, and briefly lifted £5 on USDA Thursday, and ended the week at £163.25. Strategie Grains increased their forecast of the UK wheat harvest to 15.08mt (14.88mt last year) because yields are higher at 7.6t/ha; of which 24% will be of milling quality (29% last year). DEFRA’s census for England suggests that the planted wheat area is 1.82mh (a 1.6% increase over 2010). In France >90% of the wheat has been harvested; a crop of 33mt is expected (36mt last year), of which 90% will be milling wheat. Iraq bought 50,000t of Russian wheat, and 100,000t of US wheat, good news for US - their exports have been quiet. Iraq has been hit by a drought, so its wheat harvest is expected to be only 1.73mt (2.2mt had been expected, and 1.86mt last year). There are increasing concerns in the MENA, that the Black Sea may face logistical problems in trying to satisfy recent sales, so that it makes sense to spread some of the contractual risk. Global wheat production is estimated to be 672mt this year (USDA).

The IMF reckons that the Gross Domestic Product (GDP) of the world in 2010 was $63,048bn, of which the Eurozone contributes the most at $16,282bn, the US comes second at $14,658bn, third is China at $5,878bn. So the EU and US together contribute almost 50% of the market value of all goods and services sold last year. The US has massive debt and the ramifications of the loss of its AAA status have yet to be felt. The EU is in difficulty trying to defend its currency, and its weaker members from default. The US and EU have problems with political credibility, and the markets are furious. `George Soros’ types are lining up to take a pop against the € weakest link (aka France). Like it or not, commodities are just an asset class as far as the funds are concerned, and whilst these heavyweight matters dominate the news, we can almost forget the niceties of supply and demand, weather, harvests and anything normal. Although China and Russia have been critical of the US (Russia called the US a parasite, and China was vocally unimpressed with US politics), both are long of US Treasury Bonds because holding $s prevents their own currencies from appreciating against the $ and making their exports too expensive. It is also useful to have a ’financial hold’ over the most powerful country in the world and your most important export market.

The world is hoping that the BRIC countries will provide the growth necessary to pull the world out of global recession – Brazil’s GDP is $2090bn, Russia $1465bn, India $1538bn and China $5878bn = $10,971bn which represents only 17.5% of world GDP. Essentially a small tug-boat struggling to pull a massive ocean liner. However there are signs that China is changing its strategy; owners of some $1000bn of US debt, it appears to be allowing the Renminbi to appreciate, which will slow its exports and its growth. Long term, this might be less risky than over-accumulating $ and € debt.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.