Humphrey Feeds weekly feed report - 16th July

Just as the Kansas wheat harvest nears completion, the USDA confused the market. The previous USDA report was bearish as it indicated big carry-out stocks and good plantings. Then on Tuesday it lowered the outlook for both maize and wheat supply (a ploy we suspected!). The trade was expecting a maize carry out of 1000mb, but the USDA predicted ending stocks at 31 Aug 2011 at 880mb (a 15-year low), and for the same date in 2012 at 870mb. So despite big prices for more than a year, the US will be unable to increase its stocks year-on-year due to increased demand from biofuel and China.

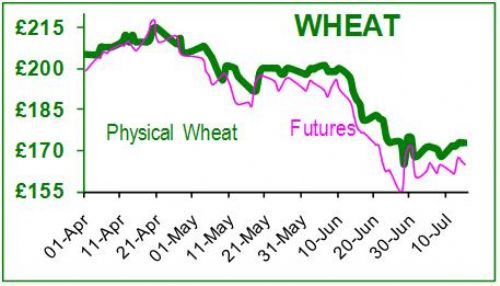

Ethanol reached a 3 year high yesterday on fears of accelerating demand against a backdrop of limited maize supplies worsened by enduring hot weather in the corn belt. Similarly wheat exports were increased by 100mb. This bullish USDA report combined with a hot weather forecast stimulated fund buying; but this was tempered by events in the EU. In the near term, the USDA’s reputation is suspect, so weather will be the biggest influence on the markets. In the EU Strategie Grains believe that rain boosted EU grain production by 6.6mt to 282mt, with wheat put at 130mt, almost 3mt more than last year. November UK wheat traded +/-£5 around £163 this week.

Russia is a very cost-competitive wheat exporter at approximately $30-100/t below anyone else, and has recently sold 150,000t to Jordan and 180,000t to Egypt. The Russian wheat harvest (June/July) is looking good and grain estimates have increased to 87-92mt after timely rain (previously 82-86mt, and only 61mt last year due to drought), of which 55-58mt is wheat. They are expected to export 17mt.

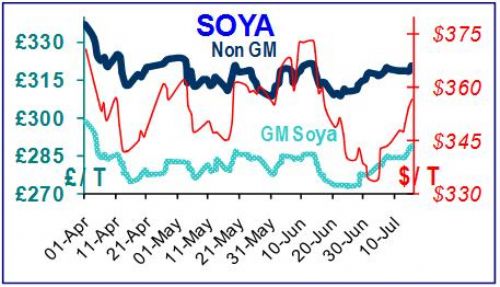

The three key worries this year have been the EU zone sovereign debt issue, a stuttering US economic recovery, and a slowing Chinese economy. ’Contagion’ was the financial EU buzz-word this week. The FT on Sunday suggested that a partial Greek default might be acceptable to some in Europe; Japanese and US funds shorted Italian and Spanish bonds and banking shares. Greece and Portugal are viewed as ’minor’ economies and almost irrelevant; however, Italy and Spain would need a rescue pot of about £1.3Tn and so are much bigger targets. Bank stress tests are another source of instability. In the US, QE3 is back on the agenda, and they have until Aug 2nd to agree a new budget, or default [a potential meltdown situation]. China’s inflation rate hit a 3-year high at 6.4% which did not go unnoticed. Chinese pork prices have risen in excess of 50% in the year to June, and people are starting to cut back on meat purchases, so China is now subsiding farmers $15 for every breeding sow. If pork prices remain high, this could ultimately limit demand for US soya. Port stocks of soya beans are at record levels of 7mt against a backdrop of falling demand from crushers, which is probably aggravated by government intervention (release of meal and oil stockpiles). The trade believes that China has already imported 5mt of maize this year; which is only 10 days consumption! China expects to harvest a record 181mt of maize this year, and has sold almost 31mt of maize from government stocks since January 2010, so it is not inconceivable that it may still need to buy 10-15mt to replenish its stores. Goldman Sachs believes in the short term US maize prices will outperform soya due to the low carry-out, but longer term believes soya has more profit potential than cereals. Spot GM soya is about £290 delivered to the mill, and £32/t more for non-GM.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.