Humphrey Feeds Commodity Report - 20/02/2012

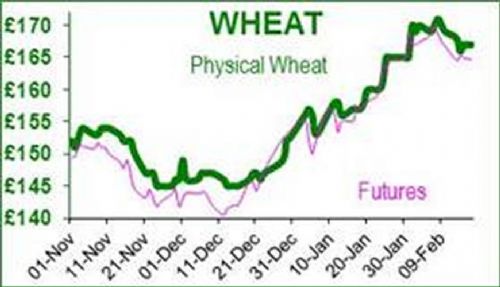

May wheat futures opened on Monday at £168 and closed at £164.60, Tuesday closed at £165.25 and more or less remained at that level over the week, until Friday when it hit £167.25. There is still talk of how much UK wheat has been exported and the potential for drought to the current crop.

Last year the NFU threatening a 30% cut in yields and we had a bumper wheat crop, and this year Caroline Spellman has already been wheeled out to talk about the drought! Speculators bought 1mt of soya on Monday (8000 contracts) so AO soya was quoted at £279 delivered to the mill early Monday morning, and by the end of the week it was almost £10 higher; in US terms this was a 4-month high. Speculators have increased their long positions in maize and soya, and reduced their wheat shorts.

The soya harvest is going well in Brazil, overall about 12% complete, and the main area Mato Grosso is about 25% complete. Southern Brazil still needs a bit more rain for the crucial pod setting phase of development, so no doubt the analysts will be downgrading the yields until it does.

Brazil may well overtake the US as the world’s largest exporter of soya this year, the peak export period will be in April. On Tuesday the bridge of a Maltese bulk ship collided with one of the four grain loaders at Santos – Latin America’s largest port – and half-detached it from the terminal, so that half of it is now underwater. A second loader may have also been damaged. As 30% of Brazil’s soya and maize are exported from this port, supplies may well be disrupted if repairs are not completed by early March. Based on history, this is also the season for stevedore strikes for higher wages.

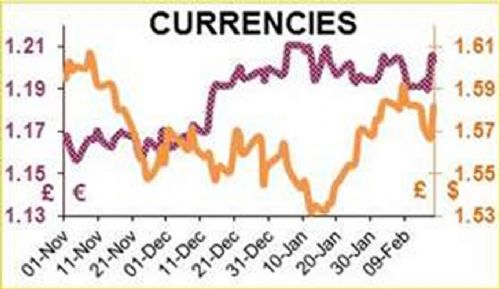

Black Sea exports are also suffering as the cold snap freezes the sea around the ports; the ice is said to be the worst for 30 years, which has slowed Black Sea grain supplies. Traders have cancelled non-ice going ships and paying $12/t more for ice-class ships to ensure shipment. The EU became export competitive for cereals due to Black Sea ice, but currency is playing havoc with exports. Much of Europe’s inland waterways have been frozen during February, so logistics are getting expensive and complicated; especially as EU feedmillers continue to buy only for the spot market.

The scenario for maize is complicated. Maize weakened at the start of the week, then strengthened with new export demand – over 1mt in a week – which was well above expectations. Technically US old crop maize supplies are tight; but wheat is plentiful. China appears to be strategically increasing its ties with South America, and following its successful soya foray, has finally concluded a deal with Argentina to start importing varieties of GM acceptable maize.

In the US, ethanol stocks are 21.5mb which is 10% above last year’s levels, and the US appears to be running out of storage space; if so then the maize-buying biofuel companies who account for about 45% of US maize demand will have to sit on their hands? If maize does get tight, then feed companies will switch to wheat, which should also limit the upper extent of maize prices.

A Chinese trade delegation has also visited the US – keep your friends close, but your enemies closer – and has agreed to buy 8.6mt of soya. This was a record tonnage for one deal. Argentina’s sabre rattling over the Falklands means that the Chinese cannot be complacent; so it is always a good strategy to keep the back doors open in case of problems with South American supply. The Chinese appear to have bought a similar amount of soya as last year, but mainly from South America to date. Soya stocks at Chinese ports appear to be high.