Humphrey Feeds commodity report - 3rd December 2011

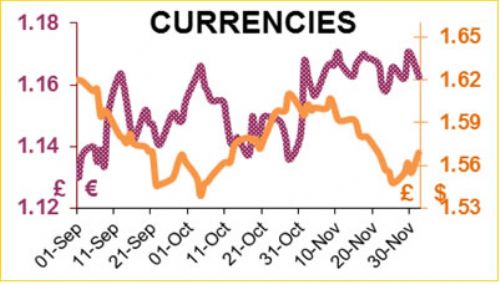

This week an avalanche of news shook the commodity markets – a UK mini-budget, invasion of the UK embassy in Tehran, OECD predictions of a recession in 2012, a UK drought, and central bank intervention to save the world. The EU Monetary Affairs Commissioner Olli Rehn escalated the crisis: ’Europe has 10 days to save the €. It is slightly concerning (to us) that the central banks collaborated to solve a problem that no-one knew existed – it is like driving on a motorway to see an ’all clear’ sign, and you just know there will be a problem ahead. The US Federal Reserve reduced the rate it charges the EU Central Bank from 1.1% to 0.6%. This shot of adrenalin boosted all markets. But for individual countries, borrowing cash at high interest rates raises the threat of insolvency, hence the need for austerity.

But the Eurozone has failed to raise the €1000bn needed for a worst-case scenario bail out, and has only €440 in its piggy bank. Now that the ECB has cheaper access to the Fed – will it or won’t it? Attention is also focussing on public sector bribery and tax evasion which is said to be at the heart of Greece and Italy’s debt problems. Apparently British Banks have £578bn exposure to the EU, and the BoE is worried. Growth rate in the BRICs is falling: Brazil cut its interest rate by 0.5%; India’s growth rate fell below 7% (the lowest for 2 years); and China’s central bank cut its reserve deposits from 21.5% to 20% to stimulate growth.

This week the Rabobank cited soya, wheat and maize as the top investment opportunities for 2012; ruling out the plunge in prices which followed the 2008 price spike because higher prices are needed to encourage planting and to counter increases in production costs. Morgan Stanley, Societe Generale and UBS made similar assertions. Goldman Sachs has a different viewpoint, and says crop futures have the worst prospects for 2012, learning the lessons from 2008. You pays your money….

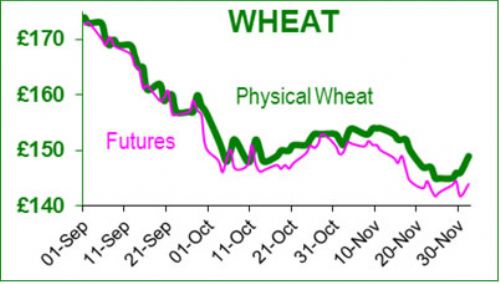

Brazilian farmers have sold out of their old crop soya, and sold almost 40% of their new crop soya (usually 25% at this time). The Chinese seem to be buying as much soya as they can from South America, so that CBOT prices are not ’stimulated’. China imported 4mt of soya in October, and the best guesses for November are 5-6mt. China has bought 15mt of soya this season (21mt at the same time last year). The US is waiting for China to place significant orders for December and January – before the Chinese New Year kicks in. The next South American soya crop (Feb/Mar) looks huge: Brazil expects to harvest 75mt; Argentina 52mt. Argentina maize harvest is expected to hit 30mt (previous record 22.5mt). Argentina has some 3mt of old crop wheat sitting in stores, occupying much-needed space for the new crop harvest (Jan); so they are intending to sell it at $15 less than Black Sea prices, and will thus take the position as the world’s lowest-cost seller of wheat. Russia notes that freight costs from Argentina to Egypt are $25 more than from Black Sea ports; so logically Spain and Portugal could be potential destinations. UK wheat is about £146/t and AO soya is about £255/t delivered to the mill.

The IGC adjusted their production figures for global wheat and maize production to 683mt and 853mt; and global usage to 679mt and 861mt respectively. Stocks are 200mt and 123mt respectively. So wheat stocks should accumulate, and maize stocks will reduce. Logically consumers should switch from maize to wheat, as price rationing of maize will make wheat cheaper. Indeed the world’s largest importer of maize, Japan, said that they might substitute 0.3mt of wheat for maize. Traditionally Japan feeds most of its 100,000t of wheat imports per annum to its monogastric industry; but pork and chicken production has increased substantially because consumers are wary of eating radioactive beef - tainted with Caesium-137 from the Fukushima nuclear plant.