Humphrey Feeds weekly feed report - 9th July

After last week’s large moves, volatility this week was more subdued with Monday-Fridday November futures closes at +GBP2, +GBP3, -GBP2, -GBP1.85, +GBP3.5. The high of the week was GBP167 and the low was GBP159. On Tuesday, a single chunk of 850 lots traded – 85,000 tonne; over the week, the Open Interest fell by about 1000 lots.

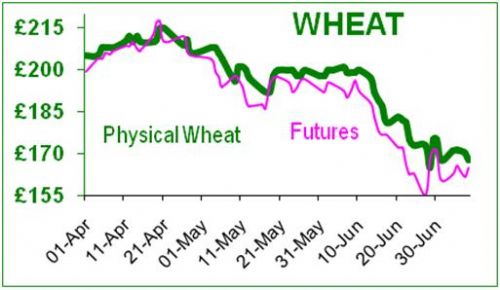

The Rabobank believe that harvest pressure, the bearish USDA report and Russian exports are weighing heavily on the market. They believe that US maize prices are now too low because investors over-reacted to ’questionable USDA data’. The USDA intends to re-survey four states so a correction is on the cards, as they have done in the past. The world’s wheat buyers are wary of buying from Russia, and this is adding more bearish pressure to Russian prices, but Egypt did succumb this week and bought 180,000t. Rain is delaying the harvest in both Russia and the Ukraine, with scare stories that the Ukraine could lose 30% of its grain in some areas were mooted as a cyclone provided 150mm of rain in 4 days. [More feed wheat then!] The Ukraine expects a harvest of 19mt of wheat, 8mt barley and 15mt maize. The EU wheat harvest has started: Spain had a good harvest in May, and France has just begun. The Chinese seem to be buying in the dips, and bought 540,000t of US maize, confirming that they are either replenishing stocks, or that their own harvest (Jul-Oct) will not be as good as predicted. The Chinese may need to buy up to 10mt of maize over the next year. The HGCA June survey for GB estimates that the wheat acreage has risen slightly and is expected to produce 14.96mt (14.88mt last year, 14.08mt the year before, and 17.23mt in 2008). Many wheat traders believe this figure is too high. For almost the entire month of June, US wheat was cheaper than US maize, but in July maize reasserted its position as the cheapest US cereal.

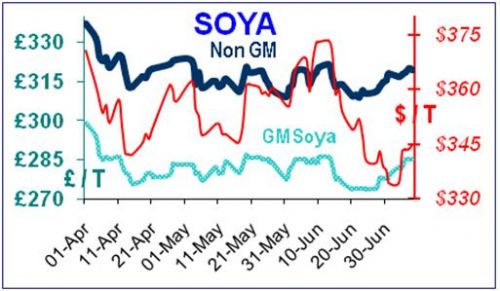

The Rabobank expects soyabean prices to firm, keeping above the $13/b level, due to the USDA’s report of reduced acreage to 75ma (2ma less than last year). Soya continues to trade in a narrow band, currently GBP282 delivered to the mill plus another GBP37/t for non-GM. The trade continues to worry about the reduced planting acreage.

This week Moody’s down-graded Portugal’s ratings which weakened the € and GBP. The US has a month of wrangling to sort out its budget deficit, otherwise its triple A rating is at risk. The European Central Bank (ECB) raised its interest rate by 0.25% to 1.5 percent, the highest since March 2009; China also increased its interest rates.

Surprisingly, Nigeria is the US’s biggest buyer of Hard Red Winter (HRW) wheat, buying 110mb (about 2.4mt) last year. They use it to make pan bread – a cheap source of staple food. The Nigerians recently commented that in terms of food, consistency of supply ensures political stability.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.