Humphrey Feeds weekly feed report - 9th October 2011

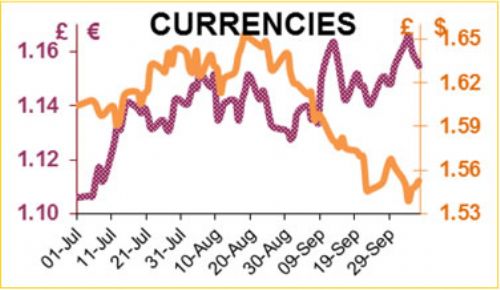

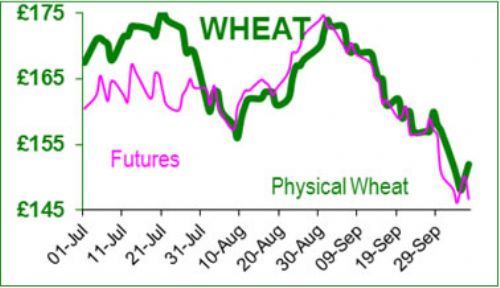

The Friday closes for November wheat futures for the past 5 weeks have been £173.05, £168.50, £161.75, £156.50, £150.65 and today £146.75. Since the first week of September, US soya bean meal has fallen from $382/short ton to $303, but as £1 has fallen from $1.62 to $1.54 over the same period, the prices of GM soya have fallen from £294 to £267. The falls were unexpected and mainly due to the recent USDA report and speculator selling, as the fundamental outlook for both maize and soya is bullish. Again, the financial world has hijacked our markets.

Goldman Sachs reduced its price outlook on the price of maize following the USDA report which stated that the US had 33mt in stock - 5mt more than expected. The USDA argued that recent higher prices had reduced usage in animal feed – a view that is contested by agriculturalists quoting livestock numbers. If the USDA were right, then feed consumption was reduced by 70% in the last six months! So the only logical explanation is that the USDA also miscounted last year’s carry-over stocks. The same arguments could also apply to UK wheat statistics, if one considers last year’s production and exports. In terms of macroeconomics, Goldman warned of a Great Stagnation and believes that a recession will occur in the EU in the next 6 months. The OECD have suggested a ’get out of jail free’ card for the EU; high commodity prices mean that arable farmers do not need EU support (CAP etc) which comprises €77bn, almost 50% of its budget.

The financial crisis continues to rumble along – like the old song ’Three wheels on my waggon’ - although the actual number of wheels is debatable. The only financial tool left in the box is Quantitative Easing, so QE2 dropped £75bn into the bankers laps on Thursday; so will QE3 be deployed in the US? In theory this gives the banks more money, makes them able to loan more, which boosts the economy; it also devalues currency which increases exports and upsets the neighbours. In practice, QE gives the banks more money to speculate on commodities, which causes price spikes, which leads to inflation, which means that people have less money in their pockets, which slows the economy. Oops! We heard the BoE say that ’this is the worst financial crisis since the 1930’s – if not ever’. David H Fischer, author of the Great Wave, analysed price spikes in the grain market from the 12th to 20th centuries, and identified four occasions in the past – in the 13th, 16th, 18th and 20th centuries where similar crises have occurred. In each of these price spikes the world also experienced crises of rising crime rates, changes in the money supply, unstable financial markets, rising public debt and lagging wages. Although written in 1996, the similarities with the current scenario are uncanny. China is not immune to a financial crisis; apparently a lack of government bank lending has forced citizens and businesses to use loan-sharks. A spectacle manufacturer has just defaulted on a £203m loan (at 80% /annum interest) by loan-sharks, and the dominos are starting to fall.

In boardrooms around the globe, there are arguments about the price of commodities. The FD will argue that in a free market all the known information is priced into the markets, so that the price of a commodity is ’discovered’ and therefore ’true’. But our markets are anything but free, they are constrained by a web of legislation, local money supply and interest rates etc, all of which varies according to what time it is on the 24-hour clock. Half of the world’s derivatives trade (futures and options) passes through London, so only half of the action happens in our office hours. Half of all stock market turnover in London and New York is generated by computer programmes – so how do computers listen to the news about the weather, crop status or earthquakes? They cannot, the programmes can only analyse the trends and look for disparities in the market, and usually operate on very short timescales (milliseconds). Computers cannot think (yet) they just process the data, so traders would argue that markets are not free, as they are skewed to the short-term and that price discovery is blurred; so there are opportunities for the brave of heart, and pitfalls the size of bear traps for the rest!

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.