Humphrey Feeds - Commodity report - 21st May 2012

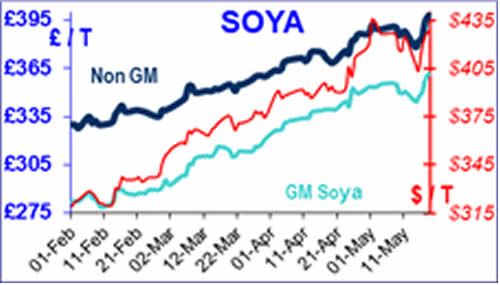

The funds started the soya Bull Run in the early part of this calendar year as a punt, when the trade could not see what all the fuss was about.

Then the South American crop numbers continued to fall, and the trade realised that there was a bigger problem than expected, and that the funds had positioned themselves well. For the past month, the raw material supply trade has been extremely bullish on soya.

On the 1st of May, AO soya hit a peak of £348/t ex port. Then last Friday, some of the funds (JP Morgan?) started to throw in the towel, and sold to realise their profits, so on Monday this week, AO soya was £335/t. Last week’s USDA report eased the old crop, and estimated China’s soya imports next year at 61mt, up 5mt from this year. Now the trade believes that the UDSA massaged the figures to ease the tightness in old crop, where cash markets are very strong.

So soya went back up again and is now £353/t, a move of £18 in a week! Argentina’s soya bean harvest is about 80% complete.

The reduced soya production from Brazil (65mt) and Argentina (42mt) means that premiums in South America are staying high, as farmers are reluctant sellers. Buyers are therefore driven to US soya (particularly China), and demand is expected to remain high until Spring next year.

Until then the markets are going to be affected by weather markets and statistics. All markets are incredibly jumpy. The one interesting factor will be to what extent US farmers’ double-crop, by planting soya after the wheat harvest.

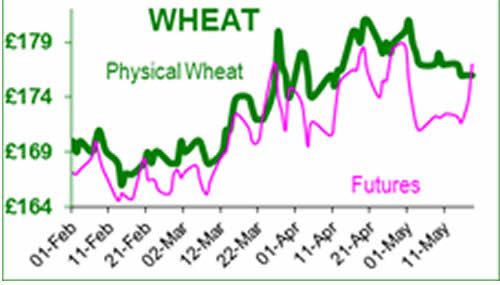

UK May futures are due to expire on May 23rd – this contract has been supportive of old crop values since mid-December; so it will be very interesting to see what happens to old crop values after its demise.

Will the July contract take over? There is currently a £30/t chasm between old and new crop, so old crop looks vulnerable.

Most of the feed and flour mill trade will have cover for old crop - you may get a slapped wrist for paying too much for wheat, but you could lose your job if you cannot find wheat and the mill stops! So prices could fall rapidly with forced sellers and few buyers.

In terms of new crop, the drought is more-or-less over so November futures hit a three-month low on Monday at £146.25, and closed Friday at £158.80, a move of >£11 in a week!

American investors appear to be concerned about dryness in the mid-west, Europe, Russia and China. Strategie grains liked the rain in the UK, but believe wet weather will increase the disease risk Some 90% of UK wheat exports are to the EU.

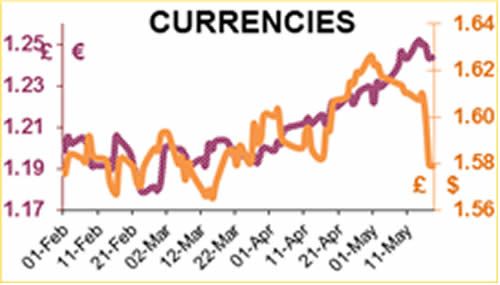

But the Eurozone’s problems have increased the strength of sterling against the €uro, which makes life more difficult for UK grain exporters – fantastic! The exchange rate is approx. £1 : €1.245, the best exchange rate since November 2008.

The financial world. The US is likely to favour QE3 at the end of June. Later this month, Moody’s is expected to downgrade the largest banks in France and Germany – BNP Paribas and Deutsche Bank AG respectively.

Politicians of the world are in a quandary - its citizens are stuck between a rock and a hard place, the world needs fixing and there are only three tools available for them to use: austerity; printing money; or deficit spending.

There are no instructions and the outcome is uncertain. Ergo, we are guinea pigs in one of the biggest economic experiments of all time. China is experiencing the start of a property collapse, house prices have fallen in 100 cities for the 8th month in a row, which does not bode well.