Humphrey Feeds weekly commodity report - 9th May 2011

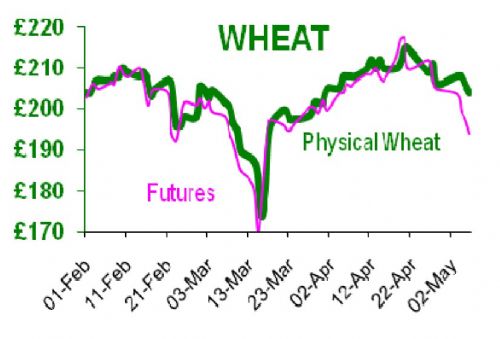

November wheat futures hit a high of £180 on 26th April, just £3 short of the contract high in early February. In the six trading sessions since then, it has fallen £16/t to £164 and is currently trading near £172. UK wheat delivered to the mill is £202.

We have been buying wheat and soya for more than 30 years, and we have stressed and sweated about the futures markets, the weather, soil moisture, currency, stocks, usage, biofuels, various world conflicts, GM issues, freight costs. But today we were informed that copper has had a very close correlation with wheat.

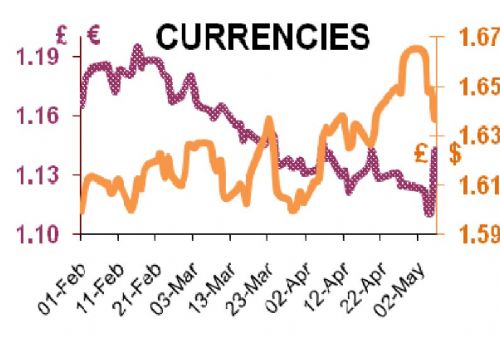

The explanation is that all the above factors have been irrelevant for the past six months, and that the only common factor between copper and wheat is fund buying and selling. So on that basis, a general selling of commodities has taken place over the past few days as investors reduced their exposure in energy, metals and grains, probably because of the rise in the $ which makes

commodities more expensive, and therefore less appealing to buyers.

The UK grain trade continues to fret about old crop stocks and new crop exports. In theory new crop exports should be limited to 1.4mt in 2011-12 as we run low on old crop carry-over – but when has that ever stopped an exporter from shipping? Especially when UK wheat is cheaper than the French by £20/t (Nov futures).

Apparently UK wheat was supplied to some unusual destinations this year: Turkey, Thailand, Vietnam and Mauritania (West Africa). Gleadell believe that wheat exports this year to June will be about 2.5mt, so that ending stocks could be a mere 1.5mt. So the focus is now on the current dry spell (my lawn is now turning brown) and the size of this year’s harvest; but rain is expected this weekend.

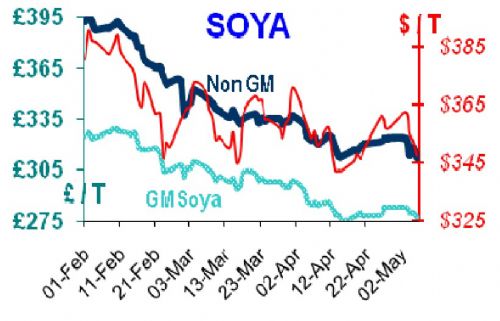

On the soya front, the Chinese have been quiet, South American harvest estimates keep growing, and at this slow rate of sales South American soya will be competing directly with US soya sales in the autumn. Soya has been trading sideways since February, but currency has improved from $1.54 to $1.64 over the same period. GM-free is now £312 delivered to the mill, and GM soya is now £276 on the same basis.

We have also been concerned about the rate of change in the biofuel world. DRAX power station burns about 400,000t of ’biomass’ which includes raw materials such as: wheatfeed, palm kernel and straw. DRAX is investing £80m to burn an additional 1.5mt, so that about 2mt of raw materials will be burned to make 500MW of electricity. The world’s biggest pelleting press has been installed to make 100,000t of straw pellets which are easier to handle and burn. The intention is to save 0.5mt of CO2 emissions a year. When added to the two biofuel plants at Ensus and Vivergo, each of which uses about 1.2mt wheat/annum, then some 4mt of raw materials are potentially being

removed from farm animal use. We do not count the waste products of biofuel, Dried Distillers Grains (DDGS), as having any real value for poultry.