Humphrey Feeds Weekly Commodity Report w/e 13-5-11

These wheat markets are incredibly volatile, and could drive a person to madness. On Monday we witnessed a rise of £9 on the November futures, apparently driven by the last day of trading the May contract on the French Matif. Tuesday added another £1.25, Wednesday dropped £3.35 after the USDA reports Thursday dropped £3.15, and Friday is up £3.50 so far. There are a myriad of factors that could push wheat and soya strongly in any direction, so most of the grain trade are sitting on the sidelines – observing the results of the funds day-trading.

Unusually, UK May futures are about £10 more expensive than July with about 100,000 tonne of Open Interest, and the indications are that most of the wheat held in futures stores is owned by one company, so the shorts are finding it difficult to buy back, creating this unusual situation. This looks like a grain trade squeeze on a massive and painful scale. Our guess is that most of the feed trade has covered until August, and so the grain trade has few opportunities to sell physical grain. In terms of new crop, November wheat futures have been bouncing between £162 and £182 since mid April, and are currently £174. It is a weather market (in China, US & EU) which is crashing into fund activity, the combination causing untoward volatility. For the past few months, it has been dry everywhere; but this week there are forecasts of rain everywhere and we expect prices to ease. The bulls continue to highlight the areas that the rain has missed. The rain in the eastern MidWest means that some farmers will miss the window for planting maize, so soya will be planted instead.

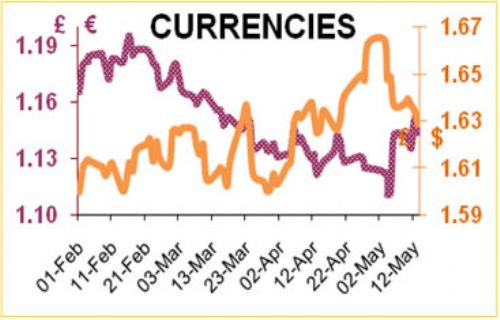

Wednesdays USDA report unexpectedly painted a rosy picture for ending stocks on maize, wheat and soya; but although the bears would like to believe it, the very political USDA are famed for their aversion to presenting bad news. So overnight the bears won, and the fears of the US running out of maize vanished, and prices fell limit down. The USDA now estimates a carryout of 730mb (about 20mt) of maize and 170mb (about 4.5mt) of soya. Brazil’s soya harvest has been lifted by 1mt to a record 73mt. China is buying less US soya because it has released oil and meal from its stores. We wonder if the Chinese are being very clever, and have withdrawn from the US market to let prices fall? In dollar terms, soya has been relatively steady at around $13.5/b, but the dollar has been trending weaker against sterling since January.