Humphrey Feeds weekly feed report - 23rd July

US maize (December futures) increased in price from a low of $5.81/b on 1st July by 20% to $7.00/b this week, mainly driven by the weather and pollination. A Chicago broker (helpfully!) believes maize prices could reach a record $8.75/b if drought persists, but could drop to $4.50/b in ideal weather conditions.

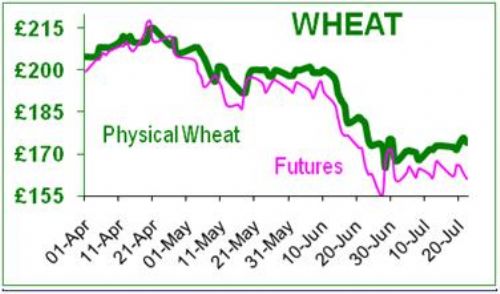

November UK wheat traded +/-£3 around £164 this week. UK wheat has tended to follow maize, but has only managed a 7% rise over the same period to about £166. Probably because the US wheat harvest is currently taking place, so supplies are plentiful. US wheat futures were also dampened by $ strength, as a stronger $ makes wheat less attractive to export; the EU debt problems could also cause less demand for US and $-priced commodities.

Russia and the Ukraine are cheap & cheerful wheat exporters and are mopping up most of the Middle East and North Africa (MENA) trade, which limits export opportunities for the US and EU. The MENA currently imports 22mt wheat per annum (2010 data), of which Egypt imports 10mt, Algeria 6mt and Morocco 4mt. These countries are only about 50% self-sufficient in terms of wheat.

By 2050, MENA will need to import over 50mt. Egypt is taking food security very seriously (for obvious reasons) and taking a chapter out of the nuclear disarmament manual ’Trust but Verify’, Egypt is relocating its grain inspectors from Egypt to Russia, to audit ships and grain quality before loading.

The UK exported 2.5mt wheat in the year to May (2.2mt last year), with some 0.62mt being purchased by the Netherlands, and 0.57mt by Spain. Surprisingly we are getting reports of a much better UK wheat crop than expected. Following the lifting of the grain export embargo on July 1st, Russia has exported 0.87mt of milling wheat (0.34mt last year) in the first 20 days of this month. And yet another pay strike in Argentina, this time by food inspectors, which is delaying 38 ships from leaving port. Soya has done very little all year, except range between $13-14/b, but possibly some excitement next month during the pod-filling stage?

Biofuels is big business in the EU with a turnover of some £11bn; it currently uses about 70% of all EU rapeseed oil to manufacture biodiesel; and 10mt of cereals to make bioethanol. This week the EU approved seven voluntary certification schemes to ensure that biofuels used in the EU are sustainable and that global biodiversity is maintained. Biofuels are essential in order to reduce CO2 emissions by 20% by 2020, but the EU do not want to be the direct cause of damage to tropical forests, wetlands or peatlands by encouraging new oil or sugar prairies. The elephant in the room is that indirect damage is entirely possible if farmers choose to grow biofuels on existing farmland, but then move their existing food crops onto newly cleared land. Clearing new land can be worse (in carbon release terms) than using fossil fuel. Greenpeace is not happy. The EU formally recognized Round Table Responsible Soya (RTRS) under one of the above certification schemes (EU Renewable Energy Directive). RTRS has developed a standard for responsible soya production that includes requirements to preserve conservation areas, to promote best management practices and fair working conditions, and compliance with the local laws.

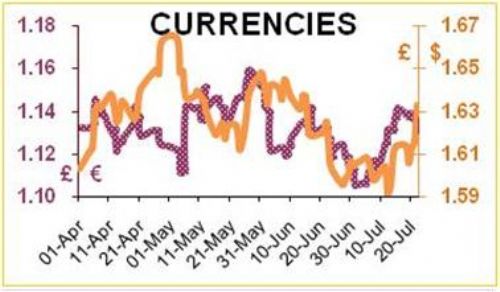

The global fear gauge crept up a couple of notches this week, as US Republicans and Democrats failed to agree on anything in the shadow of its potential debt default; and as the wealthier EU nations reluctantly supported their weaker allies in the struggle to protect the Euro. After the failure of the banks three years ago, are we about to witness the failure of some countries? The world spent billions propping up the banking system, when it might have been kinder to let some of the banks fail; so will it be ’kinder’ to let some countries fail – will we see the Drachma, Peseta, Punt and the Lira again? Whatever happens, it is more likely than not, that there will be turmoil ahead which will affect interest rates, business confidence and currency; which in turn will affect commodities.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.