Humphrey Feeds weekly feed report - 2nd October 2011

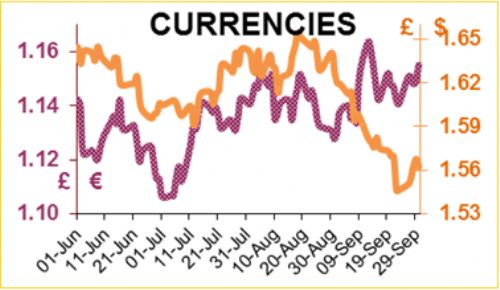

Trying to make sense of the markets during the current financial crisis, is next to impossible. The funds are still selling [dumping?] commodities; 13mt of maize has been sold in the two weeks following the 12th September, but they are still clinging on to 33mt of soya beans. [I think the CFTC should make them eat it]. On Wednesday this week, the funds sold 1.6mt soya and 2mt of maize. Soya has fallen from $14.60/b to $12.20/b in the past 4 weeks, partly due to funds and partly due to the Brazilian real weakening, making Brazilian soya cheaper than US; so US soya has had to fall? Earlier this week, maize had fallen to a three-month low at $6.30/b, soya beans hit the low for this calendar year at $12.20/b, and soya bean meal hit the lowest since 8th October 2010 at $315/short ton. Today’s bearish USDA report means that all the ’grains’ will probably stay weak until their next report on Oct 12th; UK wheat fell £6 today. A year ago today GM soya was £283 delivered to the mill (the £/$ was 1.59), today it is £272 (£/$ is 1.56). In 2001, the GM soyabean acreage in Brazil was only 16% of the total, and a decade later it is 76% (71% last year). The GM percentage in Argentina is 98%, ahead of the US at 95%. The US soya harvest has started. The soya bean supply and demand situation appears to be tight until harvest 2012, mainly because the Chinese are expected to buy about 55-60mt this year. As their pig industry continues to grow, partially supported by subsidies, their requirement for soya will only increase. Last year (2009-10) they imported 9mt more than the previous year, and this year (2010-11) 2mt more than that; a rise of 5mt is expected in 2011-12. Demand for soya could well be higher than this, as the government targets illegally reprocessed cooking oils that have caused food scares.

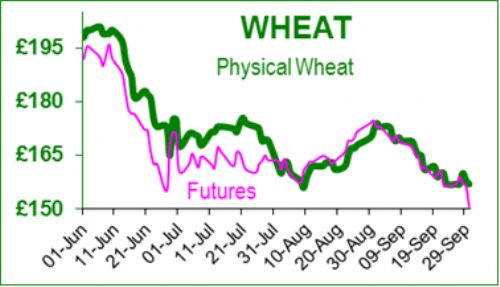

Russia is complaining that the French are becoming more competitive as world prices fall – possibly because port stocks are dwindling, forcing higher prices to attract wheat from more distant areas. Russia plans to spend £368m in developing grain terminals and transport (river, road and railway) on the Black and Baltic seas. The Russian capex is expected to upgrade capacity from 25 to 40mt/annum, and reduce handling costs by $15/t (a payback of three years!). Russia currently sells wheat at $255 (£163) FOB Black Sea. UK feed wheat is about £152 delivered to the mill.

Is African agriculture the new gold rush? China now owns productive land in 29 African countries totalling 7mha, and India owns 1mha in 17 African countries. So China (pop 1.3bn) and India (pop 1.2bn) are strategically ensuring food supplies. In terms of population density, India has 930 people/sq ml and China 360; so India’s needs are more pressing in terms of land to feed its population. Bangladesh eclipses both at 3000 people/sq ml, but cannot afford the land. The UK has 650 people/sq ml.

According to a recent Commodity report from Lloyds TSB, commodity prices have risen by 232% in the last 10 years – equivalent to 13% per annum. Over the same period shares rose 4%/annum and UK housing rose 9%/annum. In the 12 months to the end of August, silver was the top performer with a return of 119%, second was maize at 93%. And as UK wheat follows maize - that says it all. Soya was in seventh place at 42%, after coffee (64%), heating oil (50%), sugar (49%) and gold (46%). So the essentials in life are sitting in a warm house, drinking sweet coffee, watching your wife (decked out in silver and gold) making dinner (maize and soya). However, in the past 3 weeks gold has lost 20% of its value, as investors shifted for the ’safer havens’ [?] of UK, US and German government bonds.

This Commodity Report is distributed by Humphrey Feeds Ltd and is provided for information purposes only. While all reasonable care has been taken to ensure that the information contained is true and not misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as such. This report is prepared for the information of BFREPA members who are expected to make their purchasing decisions from a variety of sources without reliance on this report. Neither Humphrey Feeds Ltd nor its officers accepts any liability whatsoever for any direct and consequential profit or loss arising from use of this report or its contents. This report may not be reproduced, distributed or published by any recipient for any purpose without the prior express consent of Humphrey Feeds.