Is it now time for GM?

2012 is the 16th year in which commercial GM crops have been grown and incorporated in feedstuffs. Since the introduction of GM crops, retailers have implemented strategies to address their use, revised those strategies, and in some cases reversed them.

A brief re-cap of retailers Non GM feed policy: Removed the main source of GM content in poultry diets – soya, ignored minor GM materials – vegetable oils, amino acids, enzymes and vitamins. Therefore these Non GM diets are not really Non GM!

The main source of Non GM soya is Brazil, which originally did not allow GM to be planted, yet now it is legal and progressively more GM has been planted, to the point where the last crop harvest earlier this year was 85% GM, and next year the figure will be even higher. As the number rises, the risk of contamination increases, and already tests confirm that not all Non GM soya is as Non GM as it should be.

So, we have Non GM layers feeds that contain GM ingredients, and which may also have some GM soya.

Apart from contamination, there are other problems:

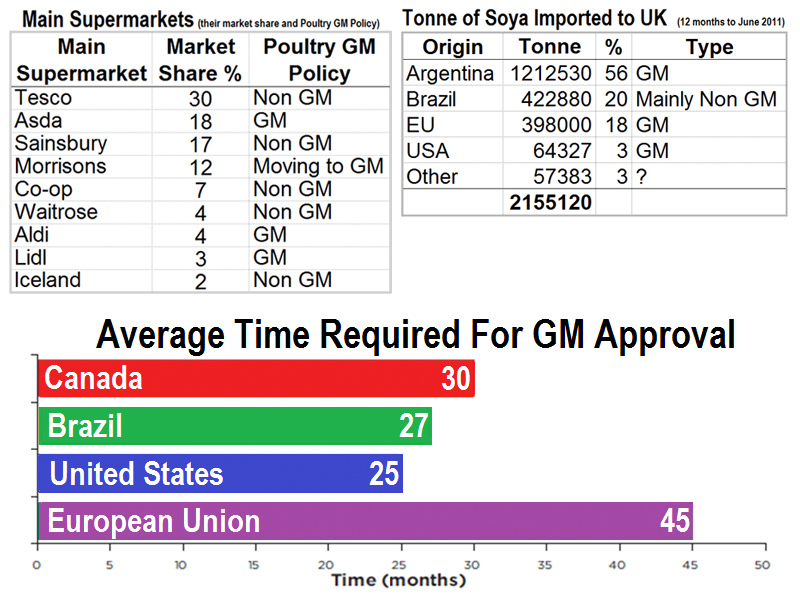

1. Asynchronous Authorisations - New varieties of GM soya are increasingly available (there are few new varieties of Non GM, so Non GM is falling behind relatively), and are approved in the US faster than in the EU. Until the new varieties are approved in the EU, they are illegal, and there is no tolerance regarding their inclusion.

As a result importers will not risk importing (potentially) more cost effective soya from origins where these new varieties are planted. (Diag. 1 shows relative delays in authorisation)

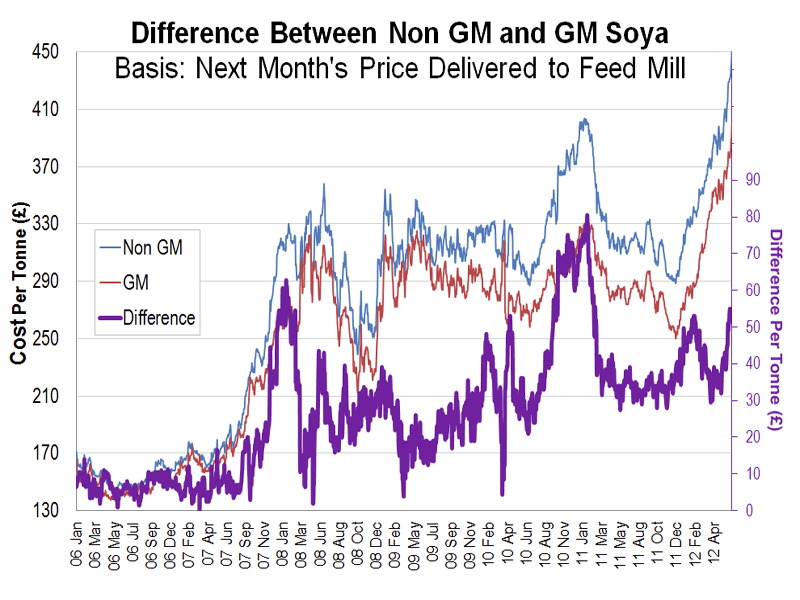

2. Price – As the performance of varieties of GM soyabeans has improved their production has become relatively cheaper, or the more outmoded Non GM varieties have become relatively more costly.

Additionally the supply chains are proving ever more expensive to try to avoid contamination, and as a result the premium for Non GM over GM has risen, and projecting into the future, it is only likely to rise further still. (Diag. 2 shows the price of GM and Non GM soya since the beginning of 2006 on the left Y axis, and the rising premium on the right Y axis)

3. Supplies – Whilst there are some supplies of Non GM to a few other EU states, the UK poultry sector is one of the few sectors for which certain retailers persist in using Non GM soya. The UK is a small market in global terms, barely 2mln tonne pa, whereas China used 55mln tonne last year alone!

At a meeting at the beginning of July, which the NFU co-hosted, and attended by oilseed producers from around the globe, it was clear that growers were perplexed about the EU’s reluctance to utilise the numerous benefits of GM.

Some of the key producing countries are turning their focus away from the EU to concentrate on the simpler markets of Asia and the Far East, rather than deal with the administrative complexity and cost of exporting to the EU. (Diag 3 shows the main sources of UK soya – whilst no figures are discernable for Non GM a fair estimate would be less than 300,000 tonne from Brazil, which would be less than 15% of all our soya)

4. Retailers – Some retailers have already changed to GM, some are thinking about it, and some want to be the last to change, but most acknowledge that they cannot implement a real Non GM policy, or maintain one in the face of mounting GM planting and contamination. (Diag 4 Shows the market share of the main food retailers, and their policy with regards to GM/Non GM).

5. Sustainability – for some retailers this could replace GM as the primary issue. Some Brazilian farmers have been accused of chopping down the rainforest to grow their soya. Whilst this may have happened at some point, the Brazilians are acutely aware of the arguments and have measures in place to protect crucial regions.

However, retailers are keen to avoid the accusation of promoting rainforest depletion, and may consider sourcing soya sustainably. There are over 400 types of sustainable soya of which RTRS soya has the highest profile. Some of these sustainable soyas are Non GM, many are GM (US soya has never been planted in a rainforest!), but all come with some sort of a premium over GM soya.

It is proving harder for retailers to maintain their insistence for the on-going use of Non GM diets, but what to do next, and when to do it are hard decisions to address. The trade that supplies farmers will already have some cover of the more expensive Non GM soya, and the importers of the soya into the UK, will have `frame’ agreements in place for the next harvest early in 2013.

Should supermarkets want to replace Non GM soya, we need to find a solution which satisfies as many people as possible, whilst keeping the costs to UK farmers competitive against the possibility of imports from our international competitors. Sustainable soya, or indeed trying to replace soya in the diet, are more expensive options than accepting the inevitability of using GM soya.

Whilst I am not personally advocating the use of GM soya, the arguments need to move beyond the ill informed and emotional points on the level of `Frankenstein Foods’, and consider the savings in costs, water usage, and bio-diversity which GM varieties are beginning to offer.

It is no longer a matter of `if’, but `when’.