Humphrey Feeds Commodity Report - 16th July 2013

Given fair weather the US maize harvest should start in mid-August – only four weeks away! The soya harvest starts a month later.

Until then prices are subject to the weather, which is currently favourable for both, but markets are extremely jittery and volatile as we hit the twilight zone between current famine and future feast. Supplies of old crop maize and soya are tight and prices high, so there is a strong incentive for farmers to sell before the new harvest year otherwise they risk losing $2 and $3/bushel respectively over the next two months.

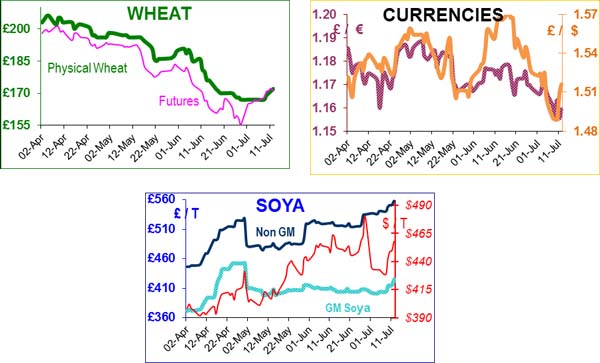

Old crop Maize futures prices hit $7.11 on the July contract (expires 12th July), whilst new crop September is $5.54, December $5.24, so the future price direction is clear beyond the technical spot position prior to harvest. Soya bean meal prices on the futures market have jumped higher again this week, two weeks ago the July contract (expires on 12th July) was trading at around $450/short ton (st), and is now at $522/st on a technical squeeze. August is $449, Sep $409, Oct $381. The EU is so short of soya bean meal, that there is talk of the EU importing soya beans and crushing themselves.

The IGC believes that global maize production for 2013/14 will be such that despite increasing demand, that year ending stocks will rise by 25%, to a 13-year high of 146mt. Total grain (wheat and coarse grains, excluding rice) production is to increase by 10% over last year, leaving ending stocks 11% higher than last year. Global soya bean production is expected to hit a new record of 284mt in 2013/14, up 6% over last year, with ending stocks up by 28%, a 3-year high. Global wheat stocks are low, Australia has more or less run out, and Argentina has closed its export programme. China bought 1.2mt of US soft red wheat last week to restock government reserves plus another 0.8mt on Monday; this follows the May purchase of 1.5mt US wheat and 200,000t of French wheat in June. Apparently they are in the market for another 1t shortly.

The party line is that prices have fallen so much that it is profitable to import and sell on; however the outside world seems to think that China’s wheat crop could be a disaster as late rains delayed the May/June harvest, causing germination in the standing crop. Reports of a good and quality harvest are being reported from the EU, and even the UK crop condition (wheat and barley) look good – with a just question mark of quantity.

Strange as it may sound, Organic soya is still grown in Argentina – mainly by default as some regions do not use pesticides nor fertilizers. We have previously reported that soya prices were so high this year that Brazilian farmers did not bother to segregate NonGM soya from GM; but this week we heard that Argentinean farmers were happy to sell their organic soya as conventional, because prices were similar and it was less hassle. If there is any logic to this crazy situation, it must be that premiums paid to farmers for NonGM and Organic soya must have to rise, which inevitably will mean that we, as buyers, will have to pay more than the current £120 and £200/t respectively over GM soya. It would therefore appear that we are being let down by our supply chain, as the ‘cake’ is being unequally divided? Port Strikes. The sailors are on strike at Argentina’s Timbues/San Lorenzo port which is hindering cereal and oilseed exports. Dock workers in Santos, Brazil are planning a 24-hour strike this week. GM is about £410ex UK port, and if you could actually buy the stuff (you cannot) Non GM soya is technically circa £140/T more.

Biofuel news. EU biodiesel production is suffering from overcapacity, and from cheaper imports. The EU’s biggest biodiesel producer (3mt/year), Diester Industrie, is reducing its French production capacity (2mt/year) by 20%. It believes that the EU will cap the biofuel inclusion to a maximum of 5%, in order to limit the impact on global food prices. This may lessen the requirement for rapeseed and sunflower seed. In the UK, the Ensus plant is still in mothballs, and the Vivergo plant is near to overcoming the last of its teething problems.