Carry out stocks of oats continue to contract in 2015/16, according to AHDB Cereals

Carry out stocks of oats are likely continue to contract in 2015/16, particularly relative to growing milling demand, according to AHDB Cereals and Oilseeds.

With a lower winter oat area indicated for harvest 2016, the level of spring oat plantings will have a strong bearing on the outlook for the UK oat market in 2016/17.

Shrinking stocks...

While the UK is anticipated to carry out larger amounts of wheat and barley than were bought into this season, the opposite is expected for oats.

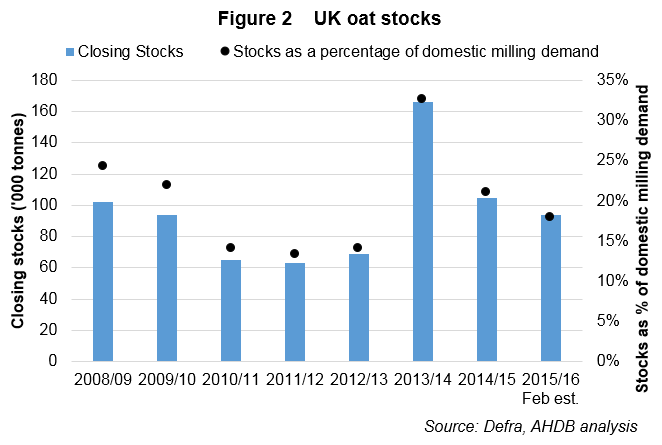

At the end of 2015/16, UK oat stocks are expected to be down 11% year on year to 94Kt, according to Defra’s latest (February) estimates.

This is in part due to a smaller crop (799Kt in 2015 vs 820Kt in 2014) but also the UK being a net exporter of oats for the second consecutive season.

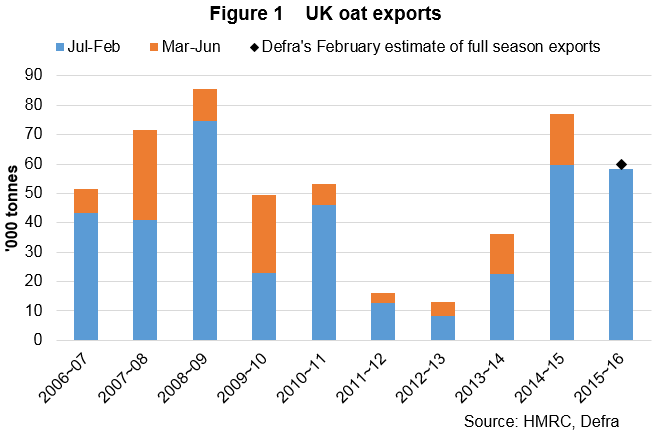

This season, exports are expected to reach 60Kt, compared to imports of 35Kt.

Furthermore, the latest data from HMRC shows that by the end of February, exports already totaled over 58Kt, or 97% of the full season forecast.

For the forecast to be met, the UK would have to export less than 2Kt from 1 March to 30 June, which has only occurred once in the past twenty seasons (998Kt in 2005/06).

Exports this season have been supported by stronger demand from Spain, which have totaled 29Kt to date – the largest volume shipped to the country since 2008/09.

There were also notable volumes (nearly 3Kt) shipped to Germany by end-Feb.

Exports are likely to exceed the current forecast and could shrink stocks further, unless another part of the market dynamic e.g. imports for animal feed demand, alters to compensate.

As a result, it will be important to monitor the export pace in the final months of the season.

…and tighter relative to demand

It’s also important to look at stocks in context of demand, in particular milling demand as unlike for animal feed, this cannot be met by any other grain.

Milling demand has grown considerably in recent years and is forecast to hit a new record this season.

Quarterly data from Defra, due for release on 5 May, will give more insight into usage so far this season (Jul-Mar) and on progress against the forecast.

Relative to milling demand, the current season carry-out stock forecast would be lower than the headline figure suggests.

It’s also worth noting that while the stocks figure relative to demand would still be higher than the 2010/11-2012/13 period, the market was particularly tight in these seasons.

As such, this reduced cushion to any potential supply issues places increased emphasis on 2016 production.

Higher reliance on spring cropping

For harvest 2016, farmers in Scotland had sown a 12% larger area to winter oats by 1 December than the previous year (Scottish government).

At nearly 9Kha, this points to the largest Scottish winter oat area in over 20 years – subject to any losses.

However, the larger winter oat area in Scotland, only partially offsets the reduction indicated to have taken place in England by the AHDB Winter Planting Survey.

Consequently, spring plantings will need to expand to prevent an overall decline in the UK oat area for harvest 2016.

Concluding comments

If current forecasts are met, the UK would arguably have cleared the stocks hangover built after the historically large crops in 2013 and 2014.

A tighter market is certainly indicated by prices (new trades) reported for near term delivery.

Since the start of the 2016, AHDB Corn Returns show spot ex-farm prices for milling oats above the equivalents for feed wheat, reducing the incentive to use oats as animal feed and indicating a market trying to preserve supplies.

With a reduced stocks cushion, the outlook for the UK oat market in 2016/17 will be heavily dependent on the 2016 crop.

Back in November, the Early Bird Survey showed the intention to expand oat plantings.

However, with a smaller winter oat area indicated for the UK, it raises the question as to whether spring oat plantings and final yields can compensate.

The next insight into the situation will be provided by the results of the AHDB Planting and Variety Survey in July.

Key points

• UK stocks set to fall 11% in 2015/16 and could shrink further if current export pace persists

• Lower stocks places increased emphasis on 2016 crop to meet demand

• Lower winter oat area indicated, can spring plantings compensate?