Humphrey Feeds Commodity Report - 8th July 2013

Generally a quiet week as the US markets took a July 4th holiday, but next week could be different as their traders all come back to work refreshed to face a new Quarter; and as the July soya meal & maize contracts expire the focus will be on the following months contracts which are a massive $60/short ton and $1.39/bushel cheaper respectively.

Last Friday’s USDA report announced lower stocks of maize, wheat and soya than the trade expected, so old crop is bullish. In terms of planting, soya maize and wheat acres were as expected at 78ma, 97ma and 56.5ma respectively, so new crop is bearish. The maize plantings are the largest acreage since 1936 when they planted 102ma. The trade had been expecting 95ma, believing the 97ma the USDA had reported in March to be a mistake, but the USDA emphatically stood by its 97ma in its end of June report. Some analysts believe that the acreage will be eventually reduced because the survey of farmers’ intentions was conducted prior to June 1st.

The crop condition report confirmed that the Hard red wheat growing States (red on map) average 17% Good/Excellent (G/E), with Kansas at 33% and Texas at 8%. As indicated in last week’s report this coincides with the drought status. The Soft red wheat States (yellow) average 70% G/E. The wheat harvest is about 50% complete. The maize condition is 67% G/E (48% last year) and the soya is also 67% G/E (45% last year). The next USDA report is the World Supply and Demand Estimate (WASDE) on 11 July. Guesstimates of the UK wheat crop for 2013 are in the region of 11-12mt compared to the 25-year average of 14.5mt.

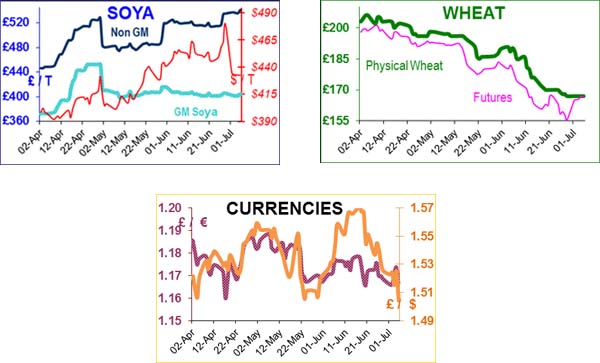

The sole UK supplier of NonGM soya has not been able to sell any for three weeks, because it has lost shipments in Brazil due to cross-contamination. Consequently all the NonGM soya it has in stock is needed to meet existing contracts for the next several months. Brazil is not selling any more NonGM soya at the moment, partly because much of it was not segregated after harvest (prices were so high anyway, there was insufficient incentive for farmers to segregate), and partly because the Brazilians are too focused on the logistics of shipping to be bothered with a niche product that is so easily damaged. Scouts have been sent worldwide to search for new NonGM, but trying to find a replacement soya of similar nutritional quality and hygiene status will be a challenge.

There are no surplus stocks of NonGM on the continent. If a new source can be found, even for delivery a few months into the future, then sales could recommence out of existing stocks. Potential supply countries include Canada, Paraguay, Uruguay and India.

Brazilian soya from its second soya crop is also a possibility. In the meantime, feedmillers are running out of NonGM so emergency contingency plans are being implemented to manufacture NonGM feed without soya. There are reports from our organic suppliers, that organic soya is being purchased because it is also NonGM. The crisis management solutions will vary from company to company, but the indications are that feeds without standard NonGM soya can cost anything from £10 to £40/t more.